Sure, it's daunting, but it's doable.

First-time homebuyers can get a foothold in Kelowna's notoriously tight and expensive real estate market if they have savings, good jobs and financial discipline.

"Potential first-time buyers shouldn't be fearful," said Clifford May, a realtor with Realty One in Kelowna.

"Yes, the cost of living is high in Kelowna, but first-time homebuyers can benefit by purchasing now before home prices go up in the spring, take advantage of being exempt from the 1% property-transfer tax and benefit by taking a five-year, variable-interest-rate mortgage that could come down as inflation comes back in check and interest rates start to drop later this year or early next year."

May is so hyped on the prospect of more first-time homebuyers that he's hosting a free First-time Homebuyer Seminar Sunday, from 2-4 pm, at the Rotary Centre for the Arts at 421 Cawston Ave. in downtown Kelowna.

Yes, Sunday is St. Patrick's Day, but May expects people to attend and get educated and inspired before they start in on the green beer.

At the seminar, May will be joined by three other professionals to give potential first-time buyers all the information they need before jumping into homeownership.

They are Balzor Singh of Anchor Mortgages, Prokopios Klimos of Daylight Home Inspections and Kirti Naslund of Summit Law.

"We're doing this as a benefit to the community," said May.

"Everyone has questions and now, with spring coming up and house buying activity and prices expected to pick up, is the time to get educated and see how first-time homebuyers can benefit by acting now."

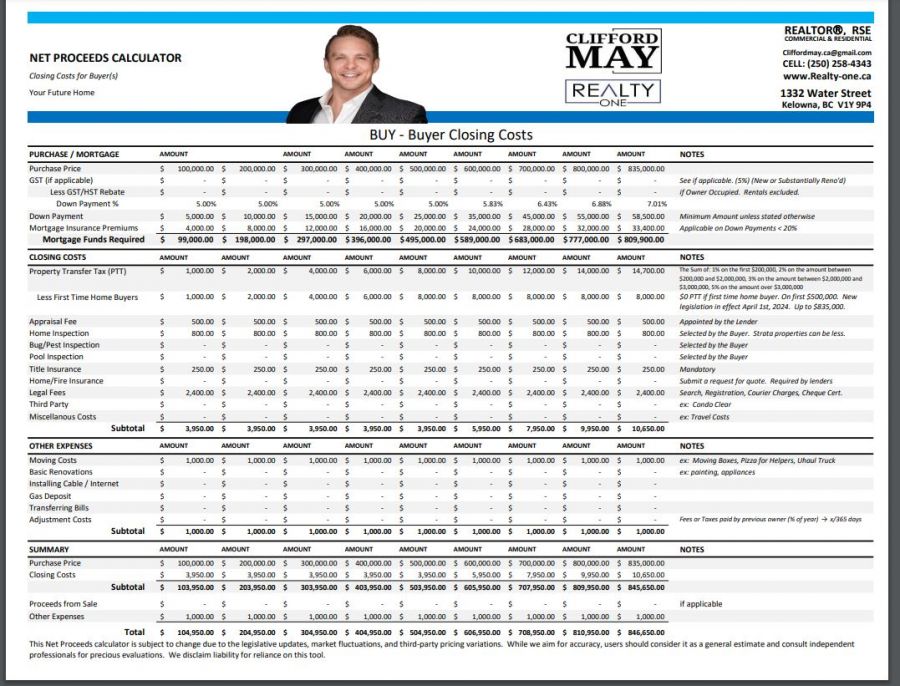

May will also hand out a 'net proceeds calculator' that outlines all the costs associated with a home purchase at various price points.

For the purpose of this article, we will use the example of a young couple buying a typical two-bedroom condominium in Kelowna for $500,000.

The minimum downpayment for a first-time purchaser is 5%, which works out to $25,000.

However, with a downpayment that low, the mortgage has to be insured to the tune of $20,000 in premiums, which is amortized into the 25-year mortgage,

So, $500,000 minus a $25,000 downpayment plus the $20,000 mortgage interest premium results in a mortgage of $495,000.

A $25,000 downpayment is a lot of money for a first-time buyer or couple and likely requires a few years of savings or a gift or loan from the bank of mom and dad.

Under new rules effective April 1 to help first-time homebuyers, they are exempt from the normal 1% property-purchase tax on the first $500,000 of a purchase.

Now, the following numbers are approximate just to give you an idea of what's needed to carry that $495,000 mortgage.

By financing that $495,000 and amortizing it over the longest term of 30 years with a five-year, variable-interest-rate term starting at 6.95%, the monthly payments come out to about $3,277.

The rule of thumb is that you should not spend more than a third of your income on housing, so your household income should be around $9,800 a month to make that $3,277 monthly mortgage bearable.

$9,800 a month income is hefty.

It works out to about $118,000 a year.

That's a lot for a single, first-time homebuyer, especially considering first-timers are likely to be younger and be early in their career and not at peak earning yet.

However, if it's a couple purchasing and each person in the couple works and makes $59,000 a year for a total of $118,000, they can swing the mortgage.

Of course, this is for a typical, two-bedroom condo, if first-time buyers want to splurge on a typical townhouse at $750,000 or a typical house at $1 million, the downpayment requirements and mortgage payments will go up.

May's 'net proceeds calculator' also makes potential first-timers aware that there will also be extra costs for an appraisal of $500, home inspection of $800, title insurance of $250, legal fees of $2,400 and however much you spend on a moving truck and movers.

Potential first-time buyers can go through the mortgage pre-approval process with a mortgage broker or bank to see exactly how much they can borrow and what all the repayment options are.

First-time buyers who purchase now can get a home priced less than it was almost two years ago at the height of the market and before prices are expected to start rising in the spring.

And once you own, history shows your home will appreciate in value over the coming years, so it becomes a sound investment that you live in.

To register for the free, First-time Homebuyer Seminar to be held Sunday, 2-4 pm, go to:

https://www.eventcreate.com/e/firsttimehomebuyerseminarkelowna

Thumbnail photos by HiveBoxx on Unsplash and Andrew Mead on Unsplash